Recently, bad banks have gained considerable attention in the banking and financial sector. These specialized entities focus on solving the problem of non-performing assets (NPAs) and distressed assets held by commercial banks. Given the challenges faced by the Indian banking sector, the concept of bad banks has been extensively discussed.

In this article, we will discuss the concept and significance of bad banks in the banking sector, particularly their role in resolving non-performing assets (NPAs) and distressed assets. We will also explore the relevance of bad banks for UPSC aspirants, providing them with valuable insights into the topic.

Why in News?

These entities will take over the initial batch of bad loans from banks, reflecting the government’s efforts to address non-performing assets (NPAs) and distressed loans. The news highlights ongoing reforms in the banking sector and aims to alleviate the burden on commercial banks caused by NPAs.

What is Bad Bank?

A bad bank is a specialized financial institution created to handle and manage non-performing assets (NPAs) and distressed assets of commercial banks. Its primary purpose is to segregate and take over these troubled assets’ burden from commercial banks’ balance sheets.

Further, Bad banks employ various strategies such as restructuring loans, selling assets, and recovering debts to maximize the recovery value of the distressed assets. By assuming the responsibility for managing and resolving these assets, bad banks help to improve the overall health and functioning of the banking system, allowing commercial banks to focus on their core activities of lending and promoting economic growth.

Objectives

The following are the objectives of bad banks:

- Separate and manage troubled assets.

- Improve the financial health of banks.

- Minimize losses on distressed assets.

- Restore trust in the banking system.

- Focus on core banking activities.

- Support economic growth and stability.

- Sell troubled assets in an organized manner.

- Reduce financial risks.

- Aid in the recovery of banks and the economy.

Bad Banks in India

In recent years, the concept of bad banks has gained attention in India as a potential solution to address the challenges faced by the banking sector. While India does not have a specific bad bank institution, there have been notable initiatives and measures taken to manage non-performing assets (NPAs) and distressed assets.

Background

Asset Reconstruction Companies (ARCs): In the late 1990s, India introduced the concept of Asset Reconstruction Companies (ARCs) to tackle NPAs in the banking system. ARCs were established under the Securitization and Reconstruction of Financial Assets and Enforcement of Security Interest (SARFAESI) Act, 2002. These companies were authorized to acquire NPAs from banks at a discounted value and aimed to recover and resolve these assets.

Prompt Corrective Action (PCA) Framework: The RBI implemented the Prompt Corrective Action (PCA) framework in 2002 to monitor and intervene in banks with high levels of NPAs and weak financial indicators. Banks under PCA face restrictions on lending and other activities until they improve their financial health. The PCA framework serves as a mechanism to address and rectify issues in banks’ financial positions.

Sustainable Structuring of Stressed Assets (S4A): In 2016, the Reserve Bank of India (RBI) introduced the Sustainable Structuring of Stressed Assets (S4A) scheme as a debt restructuring mechanism. Under this scheme, banks could convert a portion of the debt of a stressed borrower into equity, while the remaining debt was restructured to make it sustainable. The S4A scheme aimed to provide a more viable framework for resolving stressed assets.

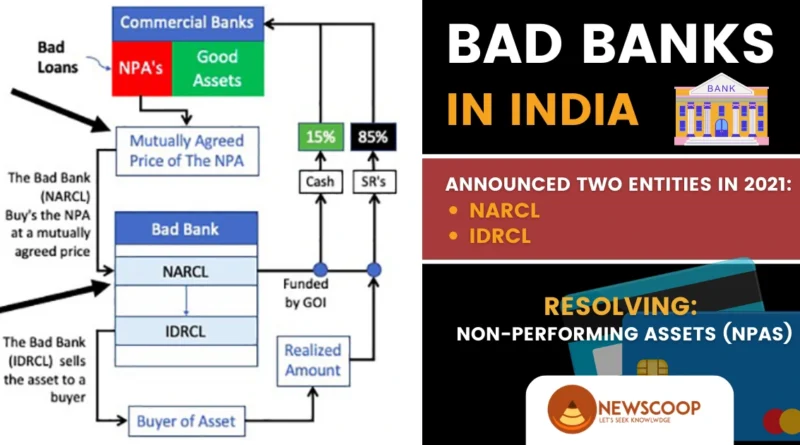

Announcement of Bad Bank: In 2021, the Indian government announced the creation of two entities, commonly referred to as “bad banks“:

- National Asset Reconstruction Company Limited (NARCL)

- India Debt Resolution Company Limited (IDRCL).

1. National Asset Reconstruction Company Limited (NARCL)

- NARCL was established under the Companies Act and has applied for an Asset Reconstruction Company license from the Reserve Bank of India (ARC).

- NARCL will purchase stressed assets totaling roughly Rs 2 lakh crore from various commercial banks.

- It will be owned by public sector banks (PSBs) to the tune of 51 percent.

- NARCL will buy bad loans from banks first.

- Payment will be made with 15% in cash and the remaining 85% in “Security Receipts.”

- Commercial banks will receive the remainder when the assets are sold, with the assistance of IDRCL.

- A government guarantee will be activated if the bad bank is unable to sell the bad loan or sells it at a loss, valid for five years.

2. India Debt Resolution Company Limited (IDRCL)

- IDRCL will be responsible for selling the stressed assets acquired by NARCL in the market.

- It will be owned to a maximum of 49 percent by PSBs and Public Financial Institutes (FIs).

- Private-sector lenders will own the remaining 51 percent of the company.

Working of NARCL & IDRCL with an Example

Let’s understand the working of NARCL and IDRCL through an example:

Acquisition of Stressed Assets by NARCL: Suppose Bank A has a portfolio of non-performing loans (NPLs) with a total value of Rs 1,000 crore. These NPLs are causing financial stress to Bank A and impacting its ability to lend and operate effectively. To address this issue, Bank A decides to transfer these NPLs to NARCL.

Valuation and Purchase by NARCL: NARCL assesses the value of Bank A’s NPLs through a due diligence process. After negotiation, NARCL agrees to purchase the NPLs at a discounted value of Rs 600 crore. Out of this, NARCL will pay 15% of the agreed price, which is Rs 90 crore, in cash to Bank A.

Issuance of Security Receipts (SRs): The remaining 85% of the agreed price, which is Rs 510 crore, will be paid by NARCL to Bank A through Security Receipts (SRs). These SRs are essentially debt instruments that represent the amount owed by NARCL to Bank A. Bank A can hold onto these SRs and receive payments as and when NARCL realizes the value from the resolution of the acquired assets.

Asset Resolution by NARCL and IDRCL: NARCL takes over the management of the acquired NPLs and begins working on their resolution. Meanwhile, IDRCL, the associated resolution company, works on selling these stressed assets in the market to potential buyers, such as asset reconstruction companies, distressed debt investors, or other interested parties.

Recovery and Payment to Bank A: As IDRCL successfully sells the assets, the funds generated from the asset resolution process are utilized to repay the remaining amount owed to Bank A. Once NARCL receives the funds, it will pay Bank A the outstanding Rs 510 crore, completing the transaction.

Government Guarantee: In case NARCL faces challenges in selling the acquired NPLs or has to sell them at a loss, a government guarantee is activated. This guarantee provides assurance to NARCL and helps mitigate potential risks associated with the resolution process.

By following this working mechanism, NARCL, and IDRCL aim to relieve banks of their stressed assets, improve their financial health, and promote the overall stability of the banking sector.

First Bad Bank

Mellon Bank, a renowned US-based financial institution, made history in 1988 by creating the first bad bank. Amid the challenges faced by the banking industry during that time, Mellon Bank took a pioneering step to address troubled assets and non-performing loans by establishing a dedicated entity known as a bad bank.

Some Other Examples of bad banks include:

- Ireland’s National Asset Management Agency (NAMA)

- Spain’s “SAREB” (Sociedad de Gestión de Activos Procedentes de la Reestructuración Bancaria).

Also Read: Small Finance Banks in India

Advantages & Disadvantages of Bad Banks

Bad banks have emerged as a solution to address non-performing loans and distressed assets in the banking sector. While they offer certain advantages in terms of asset cleanup and financial stability, they also come with their share of challenges. Let’s discuss the advantages and disadvantages of bad banks to gain a comprehensive understanding of their pros and cons.

Advantages of Bad Banks

- Asset cleanup and reduction of non-performing loans (NPLs)

- Improved financial stability for commercial banks

- Enhanced focus on core banking activities

- Potential for increased lending capacity

- Efficient management and resolution of distressed assets

- Facilitation of economic recovery and growth

Disadvantages of Bad Banks

- The potential financial burden on the government or taxpayers

- Risk of moral hazard if banks become complacent in managing risks

- Difficulty in accurately valuing and pricing distressed assets

- Challenges in achieving optimal recovery rates for troubled assets

- Potential Impact on market confidence and investor perception

- Complex operations and coordination among stakeholders.

Conclusion

In conclusion, the establishment of bad banks in India has the potential to address non-performing loans and distressed assets in the banking sector, offering advantages such as asset cleanup and improved financial stability.

However, it is important to be mindful of potential disadvantages, including the financial burden on the government and the risk of moral hazard. Effective implementation and coordination among stakeholders will be crucial for the success of bad banks in India. Ultimately, if managed well, bad banks can contribute to strengthening the banking sector and promoting economic growth.

Thank You!